Sponsored Content | Digital Free Press

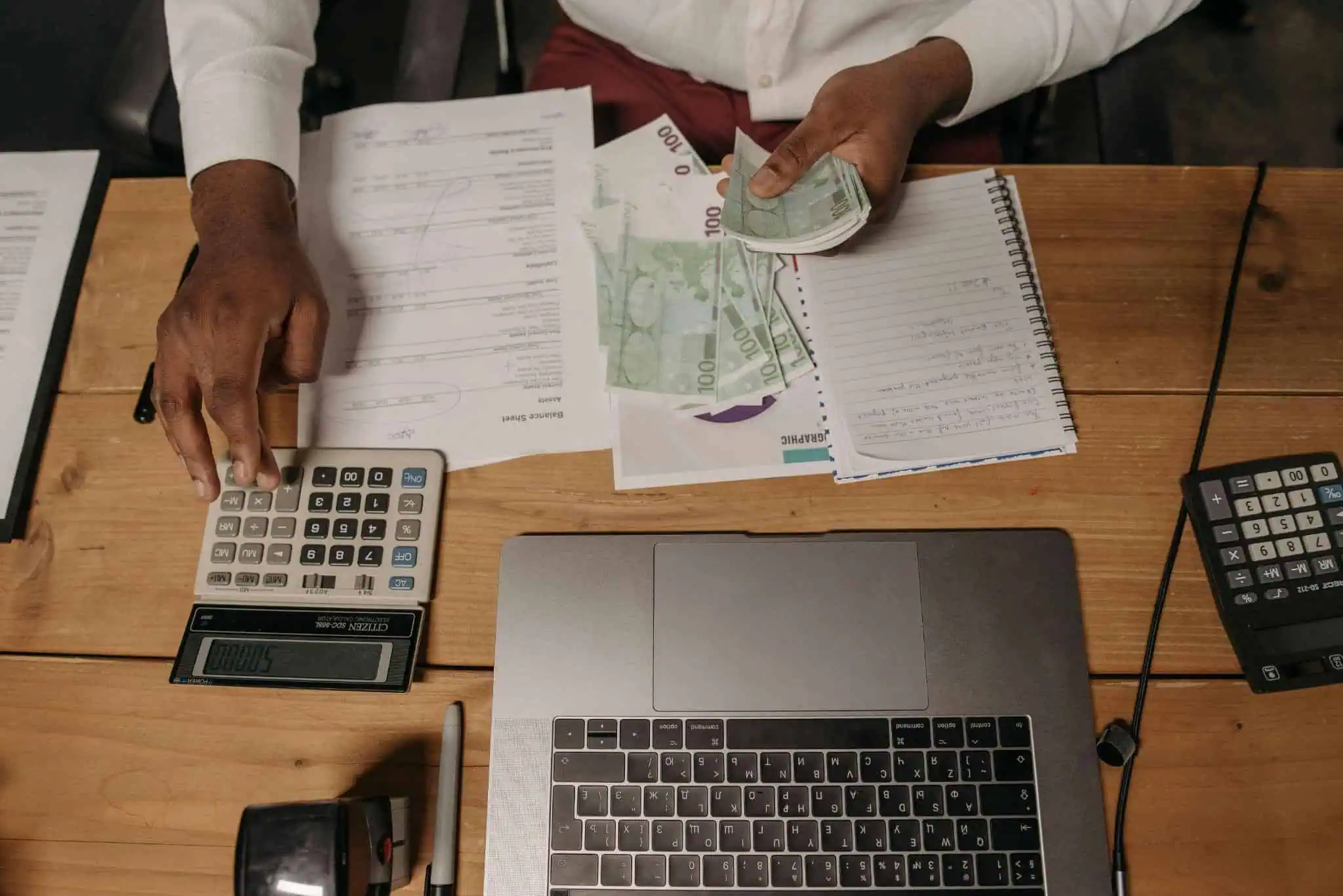

Arizona homeowners are navigating a very different financial landscape in 2026 than they were just a few years ago. While the state’s housing market continues to show resilience, rising insurance costs, property taxes, utility bills, and everyday expenses are putting pressure on household budgets across Greater Phoenix and beyond.

For many residents, the conversation is no longer just about buying a home; it’s about making homeownership more affordable long term. As a result, more homeowners are exploring mortgage refinancing as a practical strategy to improve cash flow, reduce monthly expenses, and create greater financial flexibility.

From Phoenix and Scottsdale to Mesa and Chandler, refinancing activity is increasingly tied to broader cost-of-living concerns rather than simply chasing lower interest rates. Homeowners are becoming more strategic about how they manage debt, access equity, and plan for future expenses.

Why Refinancing Is Back in Focus

During the ultra-low mortgage rate period of 2020 and 2021, refinancing surged as homeowners rushed to lock in historically low rates. That wave eventually slowed as rates climbed, but refinancing never fully disappeared. Instead, its purpose evolved.

Today, many Arizona homeowners are refinancing for reasons beyond securing a lower rate. In many cases, refinancing is being used to:

- Consolidate higher-interest debt

- Improve monthly cash flow

- Access home equity for renovations

- Adjust loan terms

- Fund business opportunities

- Prepare for long-term financial stability

With inflation continuing to affect groceries, healthcare, transportation, and utilities, households are looking for ways to regain control over monthly budgets. Mortgage restructuring has become one of the more significant tools available to homeowners who have built equity over the past several years.

In Arizona, where home values remain relatively strong compared to pre-pandemic levels, many owners are sitting on substantial equity positions that can provide financial flexibility when used carefully.

Rising Costs Are Changing Financial Priorities

The cost of living in Arizona has changed dramatically over the last decade. Rapid population growth, strong migration trends, and ongoing development throughout the Phoenix metro area have increased demand for housing and services.

Although inventory has improved compared to previous years, many homeowners are still adjusting to higher overall ownership costs.

Insurance premiums have increased in many areas due to construction costs and climate-related risks. Utility bills continue rising during Arizona’s long summer seasons, and homeowners associations in some communities have also increased fees.

For families balancing childcare, commuting costs, and consumer debt, even small monthly savings can make a meaningful difference.

That is one reason refinancing has regained attention among homeowners who may not have considered it during periods of rising interest rates.

Rather than focusing solely on rate reductions, many borrowers are evaluating how refinancing can help simplify finances and improve budgeting predictability.

Debt Consolidation Is Becoming a Major Motivation

One of the most common reasons Arizona homeowners are refinancing in 2026 is to consolidate higher-interest debt.

Credit card balances increased nationally over the past few years, and many households accumulated debt while adjusting to inflation and rising living expenses. Credit card interest rates often remain significantly higher than mortgage rates, making debt consolidation an attractive option for qualified homeowners.

By rolling certain debts into a mortgage refinance, some borrowers are able to reduce their total monthly obligations and streamline payments into one loan.

Financial advisors often caution that refinancing unsecured debt into secured mortgage debt requires careful planning, but for some households, it can provide breathing room and help stabilize finances.

This approach has become especially relevant for homeowners who purchased properties several years ago and have since gained substantial equity due to Arizona’s home value growth.

Home Equity Is Giving Owners More Flexibility

Arizona’s real estate appreciation over the past several years has created opportunities for homeowners to access equity in ways that were not available before.

Many homeowners who purchased homes before the recent housing boom now hold significant equity positions, even as market growth has moderated.

That equity is increasingly being used strategically.

Some homeowners are refinancing to fund renovations that improve long-term property value, especially as labor and construction costs continue to rise. Kitchen remodels, energy-efficient upgrades, office additions, and outdoor improvements remain common projects throughout Arizona communities.

Others are using equity to support life transitions such as college expenses, relocation planning, or launching small businesses.

In some cases, refinancing also helps homeowners shift from adjustable-rate mortgages into fixed-rate loans for greater payment stability.

The broader trend reflects a growing shift in how homeowners view their properties — not just as places to live, but as long-term financial assets that can provide flexibility during changing economic conditions.

Arizona’s Housing Market Still Supports Refinancing Activity

Despite slower price growth compared to the peak pandemic years, Arizona’s housing market remains relatively stable entering 2026.

Markets such as Scottsdale, Chandler, and parts of Phoenix continue to experience demand driven by relocation, technology expansion, healthcare growth, and business development across the region.

At the same time, inventory levels have improved compared to the extremely limited supply conditions seen in earlier years.

That combination has helped support property values while giving homeowners greater confidence in long-term equity retention.

For lenders, stable home values are important because equity plays a major role in refinancing qualification. Borrowers with stronger equity positions often have access to more refinancing options and potentially better loan terms.

This is particularly important in markets like Arizona, where homeowner migration and economic development continue to shape housing demand.

Cash Flow Matters More Than Ever

One noticeable shift in 2026 is that many homeowners are prioritizing monthly affordability over maximizing long-term investment returns.

In previous years, some borrowers focused heavily on paying off mortgages aggressively or leveraging historically low rates for investment opportunities. While those strategies still exist, many households today are more concerned with preserving liquidity and managing monthly cash flow.

That mindset is influencing refinancing decisions.

For example, extending loan terms or restructuring debt obligations may help reduce monthly expenses even if it increases total long-term interest paid over time.

For households facing rising childcare costs, healthcare expenses, or variable self-employment income, monthly flexibility can provide significant peace of mind.

Arizona’s growing population of remote workers and entrepreneurs has also contributed to this trend. Income patterns are becoming less predictable for some households, increasing demand for financial strategies that create stability and lower fixed monthly obligations.

Refinancing Isn’t the Right Fit for Everyone

While refinancing can provide meaningful benefits, financial experts continue to emphasize the importance of evaluating the full picture before moving forward.

Closing costs, loan fees, appraisal expenses, and long-term repayment timelines all matter when determining whether refinancing makes financial sense.

Some homeowners may benefit more from budgeting adjustments, debt repayment strategies, or alternative financing options depending on their individual circumstances.

Additionally, homeowners who already hold extremely low mortgage rates from earlier refinancing periods may find it difficult to secure significantly better terms today.

That is why many borrowers are focusing less on headline rates and more on broader financial outcomes such as:

- Lower monthly payments

- Reduced debt stress

- Access to equity

- Payment predictability

- Long-term cash flow improvement

For Arizona homeowners, refinancing decisions increasingly involve balancing immediate financial needs with long-term housing goals.

The Role of Financial Education

As refinancing options become more complex, financial education is playing a larger role in homeowner decision-making.

Borrowers today are researching loan structures, equity strategies, and mortgage products more carefully than in previous years. Many are comparing fixed-rate loans, adjustable-rate loans, cash-out refinancing options, and home equity products before making decisions.

Digital mortgage tools and online financial resources have also made information more accessible, allowing homeowners to evaluate scenarios before speaking with lenders.

At the same time, experts continue encouraging borrowers to work with trusted financial professionals who understand local housing trends and lending conditions.

Arizona’s market can vary significantly between communities, and refinancing strategies that work well in one area may not make sense in another.

For example, homeowners in rapidly appreciating neighborhoods may prioritize equity access differently than homeowners focused primarily on lowering monthly costs.

Looking Ahead to 2026 and Beyond

Arizona’s economy continues to attract businesses, new residents, and long-term investment, helping support housing demand throughout the state.

But alongside that growth comes higher living costs and increased financial pressure for many households.

As homeowners adapt to evolving economic conditions, refinancing is becoming less about timing the market perfectly and more about creating financial stability in uncertain times.

For some families, refinancing may help reduce debt burdens and improve budgeting flexibility. For others, it may provide access to capital for renovations, business opportunities, or future planning.

The broader trend highlights an important shift in homeowner behavior: people are becoming more proactive about managing their finances rather than simply reacting to economic changes.

In a market like Arizona, where real estate remains closely tied to economic growth and migration patterns, refinancing will likely continue playing an important role in how homeowners manage rising costs and long-term financial goals. As 2026 unfolds, homeowners across Greater Phoenix and surrounding communities are increasingly viewing refinancing not just as a mortgage decision, but as part of a broader financial strategy designed to create stability, flexibility, and resilience for the years ahead.